December 2025

Investment Memo - Nexa Resource S.A.

An integrated zinc producer left for dead by the market.

Nexa Resources (NEXA) is an integrated zinc producer, operating five mines and three smelters in Brazil and Peru. The company is one of the five largest producers of zinc globally. The company’s mines produce over 300 thousand tonnes of zinc, 30thousand tonnes of copper, 60 thousand tonnes of lead, 11 million ounces of silver, and 30,000 ounces of gold annually, and its smelters produce over 550,000tonnes of metallic zinc and over 30,000 tonnes of zinc oxide annually.

The market has left Nexa for dead due to the consensus estimate that the zinc market is likely to enter a period of surplus over the next two years and a series of operational issues that have negatively impacted its performance in the short term. We think Nexa is nearly past its current operational issues, which will allow the company to generate significant free cash flow over the next few years and reduce its current debt burden.

Zinc is primarily found in polymetallic deposits, which produce a significant quantity of byproducts. Nexa reports its financials on a per-ton-of-zinc basis, so the substantial amounts of copper, lead, silver and gold the mines produce are accounted for as byproduct credits within costs, not as revenue. This is why several of the company’s mines produce zinc at a negative sustaining cash cost, which we believe obscures the company’s leverage to higher precious metals and copper prices.

A $10 increase in the price of silver increases EBITDA by over 5% and a $100 increase in the price of zinc increases EBITDA by over 11%. Additionally, the torque to the silver price is going to increase in the second half of 2026, as a silver streaming agreement for 65% of the Cerro Lindo mine's payable silver production drops to 25%.

Cerro Lindo is an underground mine in operation since 2007, mining a polymetallic volcanogenic massive sulfide (VMS) deposit. Based on proven and probable reserves, the mine has a current mine life of around 7 years, but further exploration and the conversion of measured and indicated resources into reserves will likely extend production significantly longer. In 2024, the mines produced 86 thousand tonnes of zinc, 30 thousand tonnes of copper, 14 thousand tonnes of lead, 4.27 million ounces of silver and 5 thousand ounces of gold.

El Porvenir is a polymetallic underground mine; it is part of the Cerro Pasco Complex alongside Atacocha. Currently, the Cerro Pasco Complex is undergoing an integration project that will extend the life of mine by approximately 15 years. Based on proven and probable reserves, it has a mine life of 12 years, but we expect this to increase substantially once the Cerro Pasco integration project is completed. In 2024, the mine produced 50 thousand tonnes of zinc, 290tonnes of copper, 27 thousand tonnes of lead, 4.64 million ounces of silver and8 thousand ounces of gold.

Atacocha consists of two mines: the underground mine and the San Gerardo open-pit mine. The underground mine has been suspended since June 2020 as part of a cost-reduction program implemented in response to the COVID-19 pandemic. Atacocha shares the same skarn deposit as the El Porvenir mine. The open-pit mine has only 4 years of reserves on a proven and probable basis, and the remaining higher-grade underground mine will be integrated into El Porvenir as part of the Cerro Pasco integration project. In 2024, the mine produced 10 thousand tonnes of zinc, 12thousand tonnes of lead, 1.2 million ounces of silver and 9 thousand ounces of gold.

Vazante is an underground and open-pit polymetallic mine located in the Brazilian State of Minas Gerais. Vazante is one of the largest epigenetic zinc silicate deposits in the world. The mine's life based on proven and probable reserves is 7 years, with a significant opportunity for expansion of the resource base; we think the mine's life will be extended considerably over time. In 2024, the mine produced141 thousand tonnes of zinc, 950 tonnes of lead and 470 thousand ounces of silver. In the first quarter of 2025, a support pillar in a high-grade stope collapsed, restricting access to some high-grade areas from the mill feed. This depressed the head grade, reducing production at the mine in the first half of the year. As of the third quarter, operations have normalized, and we think that this geotechnical issue is largely in the rearview now.

Aripuanã is Nexa’s newest mine, having just commenced commercial operations in June 2024 after a 2-yearramp-up phase. The mine has over 15 years of proven and probable reserves. In2024, the mine produced 31 thousand tonnes of zinc, 5 thousand tonnes of copper, 13 thousand tonnes of lead, 1 million ounces of silver and 14 thousand ounces of gold. Aripuanã has experienced operational issues with tailing processing during the rainy season, resulting in production below the run rate.

Cajamaruquilla is one of the largest zinc smelters in Latin America and the only zinc smelter in Peru, with a nameplate capacity of 344.4 thousand tonnes per year using Roast-Leach-Electrowinning technology. In 2024, it produced 327 thousand tonnes of refined zinc, with 31% of the zinc contained in concentrate processed coming from Nexa’s Peruvian mines and the remaining being sourced from third parties and secondary feedstock.

The Tres Marias smelter processes zinc silicate concentrates from the Vazante mine and now also treats zinc sulfide concentrate from Aripuanã. It has a nameplate capacity of 192.2 thousand tonnes of refined metal per year. In 2024, it produced 180 thousand tonnes of zinc metal and oxide, with 88% of zinc contained in concentrate processed coming from Nexa’s mining operations.

The Juiz de Fora smelter produces zinc from sulfide concentrate and secondary sources. It has a nameplate capacity of 96.9 thousand tonnes per year, using a Roast-Leach-Electrowinning and Waelz Furnace technology. In 2024, the smelter produced 83 thousand tonnes of refined zinc, with 56% of zinc raw material processed by the smelter sourced from Nexa’s mining operations.

The smelter experienced a fire in December 2024, which shut down the roasting plant, resulting in a 42% decrease in production in the first quarter of 2025. Full capacity was reached again in September 2025.

Global annual zinc demand is a bit over 13 million metric tons. Over 50% of zinc demand globally comes from galvanizing steel. Another 17% of demand comes from alloys like brass and bronze, 15%-20% comes from die casting, with the remaining demand coming from the chemicals industry. Galvanizing is by far the primary driver of zinc demand. Galvanizing steel involves applying a protective coating of zinc to steel to prevent corrosion. Galvanization is the most cost-effective way to protect steel against corrosion, and while there are alternative coatings for corrosion resistance, they are often niche applications that cost significantly more. Zinc is commonly found in polymetallic deposits, and around20% of zinc production is mined as a by-product of copper and lead mining, and around 30% of the annual refined zinc supply comes from recycling.

The zinc market has been bifurcated as of late, with an oversupply of zinc concentrate in China and a deficit outside of China. Warehouse stocks on the London Metals Exchange (LME) have plummeted this year to around 40,000 tonnes in the third quarter, while inventories on the Shanghai Futures Exchange (SHFE) have surged to98,000 tonnes. The arbitrage window for Chinese smelters to profitably export refined zinc overseas is currently open, but we expect the price spread between the LME and the SHFE to narrow, and this arbitrage opportunity to close as inventories balance between China and the rest of the world.

The current market narrative is that the zinc market will have a sustained surplus over the next 2years due to increased mine production and a decline in global industrial activity, particularly in China, driven by tariffs and the ongoing tepid Chinese economy.

We think the consensus is incorrect. While the supply and demand balance in the zinc market in 2026 will not see the same zinc concentrate deficit we saw in 2025, we think the market is overly optimistic about the increase in zinc mine production in2026. The largest components of this predicted increase in production come from the Ozernoye mine in Russia, the Mehdiabad mine in Iran, the restart of the Tara Mine in Ireland, and the debottlenecking project at the Kipushi mine in the DRC. Of these, we think only the Tara mine and Kipushi are likely to match market expectations for zinc production.

The Ozernoyemine has faced significant delays after a 2023 fire destroyed some essential western-supplied equipment, and subsequent sanctions have made it impossible to replace these components, forcing the use of domestically designed equipment. We expect the mine to continue to face production challenges in reaching its designed capacity. The Mehdiabad mine is likely to see some production uplift in 2026, but we think its zinc concentrate will continue to face limited market access due to its Iranian origin and will not affect ex-China inventories.

We also see declines in zinc production as Glencore’s Lady Loretta mine, part of the Mount Isa complex, reaches depletion in 2026. A further decrease of 38,000 tonnes is expected in 2027 with the depletion of the Kidd Mine in Ontario. Zinc production at Antamina in Peru is also expected to decline significantly in2026 as the mine targets zones with lower zinc grades.

On the demand front, we think the market is overly pessimistic. This year, the Chinese Communist Party (CCP) drew attention to a raft of so-called anti-involution policies, which aim to curb the price wars and overproduction common in various industries in China. We think these policies will ultimately come to nothing, as did the 2015-2016 supply-side reforms aimed at reducing overcapacity in industrial production. The problem for the Chinese economy is that non-economic overproduction in industries like renewable energy manufacturing, petrochemicals, and steel keeps the unemployment rate artificially low. In order for the CCP to be serious about this new wave of anti-involution policies, they have to be willing to see the unemployment rate skyrocket, which we think they have shown themselves unwilling to do time and time again.

Additionally, we think trade tensions between the US and China will abate somewhat in 2026,as the Trump administration, looking ahead to the midterm elections, is more hesitant to intensify the tariff war. The topic of affordability has taken center stage in political discourse as of late, and we think it will remain a core concern for voters heading into the midterm elections. We think an easing of trade tensions will boost Chinese economic growth. Due to these factors, we expect global zinc demand to increase marginally by about 1% in 2026.

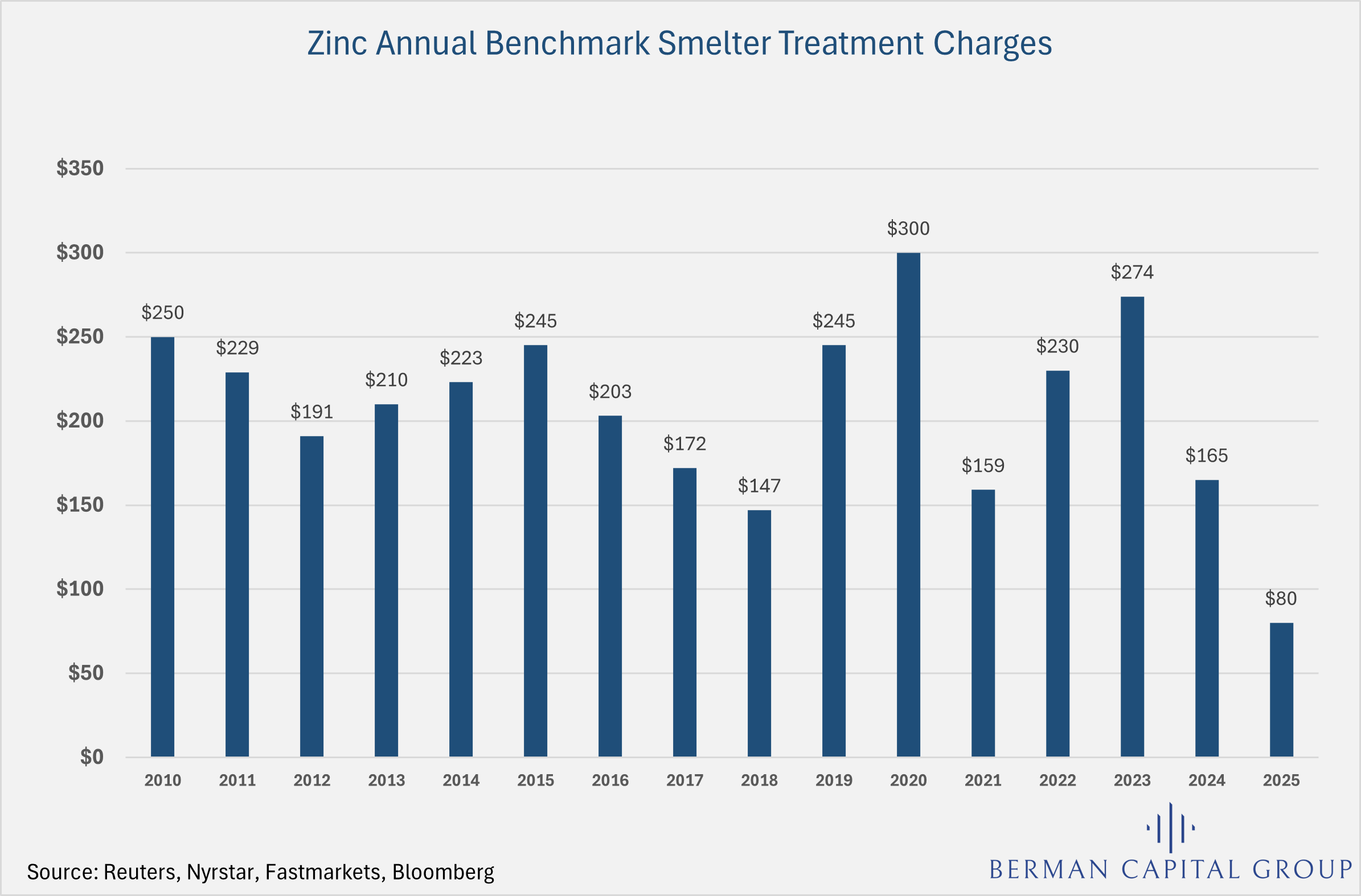

Treatment charges (TC) are the fees (usually measured on a per-ton basis) that mines pay to smelters for processing their concentrate into refined metals. The annual negotiations between Teck Resources, the operator of the Red Dog zinc mine in Alaska, and Chinese smelters have historically served as the benchmark for annual TC rates contracting. There is a spot TC rate market, but the volumes of zinc processed at spot rates are substantially smaller than those locked up under an annual contract.TC rates are determined by the balance between the supply of zinc concentrate and smelting capacity. When concentrate supply exceeds smelting capacity, TC rates rise, and when concentrate supply is low relative to smelting capacity, TC rates fall.

In 2025, TC rates reached a 50-year low of $80 per tonne. We expect benchmark TC rates to increase in 2026 due to additional zinc concentrate supply. Already, spot TC rates have increased to over $100 per tonne. Nexa uses the benchmark TC rate for its intersegment sales, but for third-party concentrate supply, it uses a rolling three-year average TC rate to reduce year-to-year volatility.

While we expect zinc concentrate supply to increase in 2026, we also expect zinc smelter capacity to increase. 2026 will be the first full year of operation by the Huoshaoyan zinc smelter in China, capable of producing 560,000 tonnes of zinc annually. We expect to see a further ramp-up in production from the Verkhny Ufaley smelter in Russia, which has a nameplate capacity of 120,000 tonnes annually but will likely produce only 80,000 tonnes in 2025. Boliden’s Odda smelter will also begin the ramp-up of its expansion project, which is expected to add a further 150,000 tonnes of annual production capacity.

Nexa’s management sees the 2026 benchmark rising to between $130 - $180 per tonne. We think that the lower end of this estimate is more likely, as TC rates will remain under pressure as we expect zinc concentrate volumes to underdeliver the market consensus in 2026.

We expect silver to remain in a structural deficit for at least the next 2 years. 2026 will be the silver market’s fifth consecutive year of supply deficit, which will continue to put upward pressure on prices.

More than 70%of the silver mined annually is a by-product of other metal mining, meaning that a higher silver price does not incentivize increased production in the same linear fashion we see for commodities like copper or crude oil. Because of this supply and demand dynamic, even though prices have increased substantially this year, we expect global mined silver to remain roughly flat year over year for 2026 and 2027.

Silver demand is bifurcated between its roles as a monetary metal and its growing industrial applications. Around 30% of annual silver demand comes from investments; silver, like gold, is seen as a store of value that protects investors against currency debasement. Industrial demand accounts for nearly 60%, with demand from jewelry covering the rest.

The growth driver of silver demand comes from its use as an industrial metal in photovoltaics. Despite the solar industry's efforts to reduce its silver consumption, silver remains essential. Most of the other materials being developed to replace silver have performance issues or add manufacturing complexity that negates the cost savings from using a metal cheaper than silver. Solar panel manufacturers have found success in reducing the amount of silver used in each panel, but growth in solar panel production has effectively canceled out the decrease in demand that would have resulted from these efficiency gains. We expect continued gains in silver demand from the solar industry, though at a significantly slower pace than in recent years.

Investment demand for precious metals often has the opposite effect of what one might expect; as prices rise, investors fear missing out on a larger run-up, so demand tends to increase with higher prices rather than fall. We see demand for silver bullion, especially from retail investor-oriented exchange-traded funds, increasing significantly in 2026.

65% of Nexa is owned by Votorantim. Votorantim, founded in 1918, is a permanently capitalized investment vehicle controlled by the family of José Ermírio de Moraes. Over five generations of the family, ownership has been spread out among 53 family members; the exact distribution of control is not publicly disclosed. While the family controls the entity and sits on the board, the firm is run by non-family investment professionals. Votorantim owns a portfolio of investments, both public and private, across a diverse array of sectors, including cement, financial services, pharmaceuticals, energy, steel, infrastructure, and even the world's largest producer of orange juice. In 2024, the company reported profits of $156 million and revenue of $9.7 billion, and it boasts an investment-grade credit rating from all three major rating agencies. While this level of ownership concentration is undoubtedly a concern, Votorantim has shown no inclination to sell its shareholding and has allowed Nexa’s management to operate independently.

The Aripuanã mine has the potential to be a very good asset, but thus far, project execution has been poor. Management’s first mistake was proceeding with the project during the height of the COVID-19pandemic-related restrictions, resulting in construction delays, supply chain issues, and reduced on-site engineering oversight. Due to supply chain constraints, trade-offs were made in the tailings plant design, resulting in the installation of three undersized tailings filters.

The three tailings filters' capacity has proven insufficient for the mine’s nameplate throughput, especially during the rainy season when additional moisture content of the tailings increases the throughput demands of the filters.

The decision was made to install a fourth, higher-capacity filter to allow the mine to operate at its nameplate capacity even during the rainy season. Commissioning of the new tailings filter will be completed in March or April of 2026. Once the fourth tailings filter is commissioned, we expect the mine to reach its nameplate capacity of 65–70 thousand tonnes of zinc per year and sustaining cash cost after by-product credits to drop to $200 per tonne of zinc, a substantial improvement from the almost $3,000 per tonne of zinc we expect costs for 2025to be.

The Cerro Pasco Integration Project is a brownfield expansion project to integrate the El Porvenir and Atacocha mines. The project is expected to increase zinc concentrate production at Cerro Pasco by 30-40%, extend the mine life by 15years, and provide additional feed for the Cajamaruquilla smelter.

The project consists of two phases, with phase 1 including the construction of a 6kmtailing pipeline from El Porvenir to Atacocha’s tailings storage facility, as well as raising the height of both sites' tailings dams. Phase 2 includes the connection of Atacocha’s underground mine with El Porvenir by way of a 2.3kmtunnel and upgrades to a shaft at El Porvenir to hoist the additional volumes coming from the Atacocha underground mine. Phase 1 is expected to be completed at the beginning of 2027, and Phase 2 is expected to be completed in 2028. The company expects to spend around $140 million on the project, $90 million on Phase 1, and $55 million on Phase 2.

This integration project is essential for extending the Cerro Pasco complex’s mine life and for accessing higher-grade ore in the Atacocha underground mine. Management believes the project will generate a return on invested capital of over 50%. Even assuming cost overruns, we think the project is by far the lowest-cost way for Nexa to meaningfully increase zinc production in a reasonably short time frame.

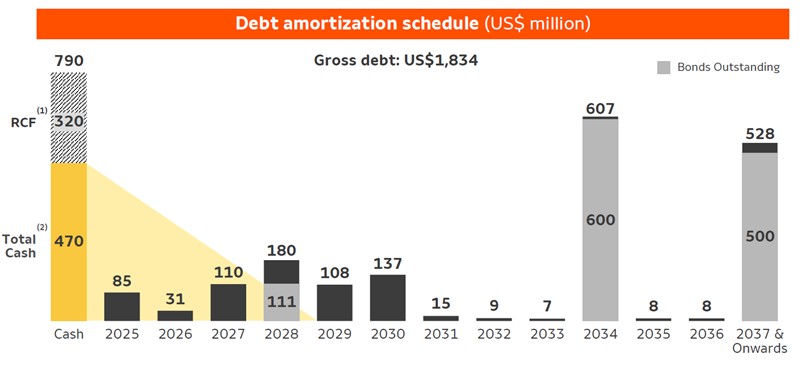

The main risk factor for Nexa is its debt burden. At the end of the third quarter, the company had total debt of $1.95 billion and net debt of $1.48 billion. The high outstanding debt has certainly scared some investors away. We do not expect the company to face any financing issues in the short term. At $130 million in annual interest expense, they have enough liquidity to cover interest payments in all but the most dire of outlooks for the zinc market.

Management has made reducing debt a priority. In April 2025, the company refinanced its 2027notes into a $500 million 12-year bond at a 6.6% coupon and tendered for 72% of its outstanding 2028 notes. We expect management to take further steps in 2026to reduce its net leverage.

The management team has shown themselves to be competent enough operators, although not all-stars. Because of this, we think it is safe to assume that construction projects will take longer than expected, and operational hiccups that temporarily reduce output are to be expected.

Even discounting the management team's imperfect execution, we still think the market is overly pessimistic about this company's outlook.

Labor relations are also always a risk in the natural resources sector; about 76% of Nexa’s employees are covered by collective bargaining agreements. We factor in the possibility of a brief strike, usually lasting no more than a week, at least once a year, since the collective bargaining agreements are renegotiated annually.

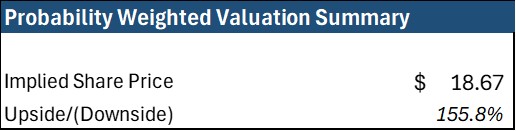

We think the market is pricing in a far worse outlook for zinc and silver than our proprietary supply-and-demand models suggest, as well as far worse operational execution by Nexa’s management team. The market seems to have completely discounted the production uplift from the fourth tailings filter at Aripuanã and the likely increase in value from the Cerro Pasco integration project.

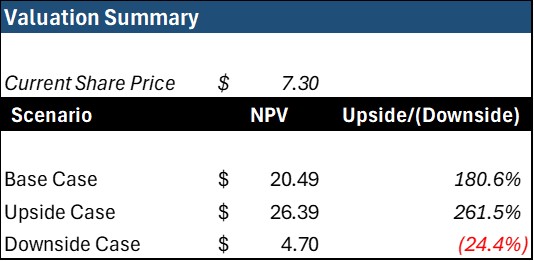

Our base case assumes the zinc price remains anchored at $3,000 per tonne, averaging around$2,800 per tonne in 2026 and 2027, and silver prices in the $45-$50 per ounce range. On the operations side, we factor in some delays in the installation and commissioning of the fourth tailings filter at Aripuanã, with full production uplift not realized until the fourth quarter, and a larger-than-guidance decrease in production at El Porvenir during the shaft upgrades for the Cerro Pasco integration project.

Our downside case assumes zinc prices face pressure, dropping to $2,600 in 2026 and $2,500in 2027. Silver prices we model dipping back into the high $30s per ounce. Operationally, we assume that even after the installation of the tailings filter, Aripuanã still has operational issues that keep production below run rate, and that the increase in production from the Cerro Pasco project is underwhelming.

Our upside case assumes the same zinc price environment as our base case and a silver price of$50 per ounce. Operationally we assume perfect execution, no delays in the tailing filter commissioning, and hitting the high end of guidance for 2026.

We based our valuation on the company's proven and probable (2P) reserves, since we have found that for companies like Nexa the market rarely assigns any value to measured and indicated reserves, let alone inferred. We think there is a high level of optionality that investors are getting for free in the continued expansion of the reserves. If the measured and indicated reserves are eventually upgraded to proven and probable, that would increase zinc reserves by 20% and silver reserves by 25%. While all current measured and indicated reserves are unlikely to be upgraded to proven and probable, this indicates the additional value that exists; the company has grown its reserves by 85% since2012, and we expect continued success given the substantial opportunity for brownfield exploration around its existing assets.

We think our investment in Nexa sets us up with multiple ways to win. The metal price and the operational execution are independent variables, and we only need to be right on one for a positive outcome.

Opinions expressed herein by the author are not an investment or vote recommendation and are not meant to be relied upon in investment or voting decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC or CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable but have not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. Funds the author advises may own shares in the securities discussed and may buy or sell shares without any further notice. This is not a solicitation or recommendation to vote for or against the transaction discussed. The note does not constitute an offer to sell, or a solicitation of an offer to purchase, any securities. Any such offer or solicitation will be made in accordance with applicable securities laws. The note is being provided on a confidential basis solely to those persons to whom this quarterly note may be lawfully provided. It is not to be reproduced or distributed to any other persons (other than professional advisors of the persons receiving these materials). It is intended solely for the use of the persons to whom it has been delivered and may not be used for any other purpose. Any reproduction of the quarterly note in whole or in part, or the disclosure of its contents, without the express prior consent of Berman Capital Group LLC (the “Company”) is prohibited. No representation or warranty (express or implied) is made or can be given with respect to the accuracy or completeness of the information in the quarterly note. Certain information in the monthly note constitutes “forward-looking statements” about potential future results. Those results may not be achieved, due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors. Nothing contained herein shall be relied upon as a promise or representation whether as to past or future performance or otherwise. The views, opinions, and assumptions expressed in this note are subject to change without notice, may not come to pass and do not represent a recommendation or offer of any particular security, strategy or investment. The note does not purport to contain all of the information that may be required to evaluate the matters discussed therein. It is not intended to be a risk disclosure document. Further, the note is not intended to provide recommendations, and should not be relied upon for tax, accounting, legal or business advice. The persons to whom this document has been delivered are encouraged to ask questions of and receive answers from the general partner of the Company and to obtain any additional information they deem necessary concerning the matters described herein. None of the information contained herein has been filed or will be filed with the Securities and Exchange Commission, any regulator under any state securities laws or any other governmental or self-regulatory authority. No governmental authority has passed or will pass on the merits of this offering or the adequacy of this document. Any representation to the contrary is unlawful.